Is Klarna safe? What to know before you buy now, pay later

Klarna is generally considered safe to use. It’s a legitimate payment service trusted by major retailers, and it uses standard security measures to help protect transactions and personal data.

However, as with any buy now, pay later service (BNPL), it’s important to track payment dates and total spending, since missed payments, late fees, or credit impacts may apply.

In this article, we explain how Klarna helps protect payments and personal data, as well as the key considerations to keep in mind before using the service.

What is Klarna?

Klarna is a financial technology company founded in Sweden. Its Swedish banking entity, Klarna Bank AB, has held a full banking license since 2017. Globally, Klarna is best known for BNPL services, which let shoppers buy from participating retailers and either pay in full later or split the cost into smaller payments over time.

It’s currently available in 26 markets worldwide and is accepted by over 1 million merchants, including Walmart, Macy’s, Sephora, Nike, and Best Buy.

Beyond payments, Klarna offers tools to track purchases, manage upcoming payments, compare prices, earn cashback, and find deals through its app and browser extension.

How Klarna works

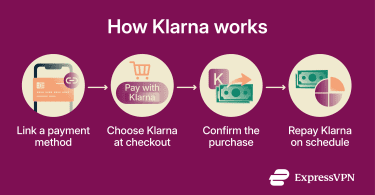

Klarna usually requires users to link a payment method, such as a debit card, credit card, or bank account, depending on the payment option and location. When you select Klarna at checkout, Klarna handles the payment with the retailer, and you repay Klarna according to the payment plan.

You can choose to repay Klarna in one of the following ways:

- Pay in 4: You split the cost into 4 interest-free payments, paid every 2 weeks. The first payment is due at checkout, while the remaining three are charged every two weeks.

- Pay in 30 days: You pay the full amount within 30 days, often starting from when the order ships.

- Pay over time: You spread the cost over monthly installments. Terms vary by country and plan; in the U.S., Klarna lists 3 to 24-month options.

Klarna’s Pay in 4 and Pay in 30 days options are generally interest-free and fee-free when paid on time, though terms and possible fees can vary by country, product, and purchase type. Pay over time may include interest or additional charges, depending on your plan.

Klarna also offers a Pay in full option that lets you pay the full purchase amount immediately at checkout. This is useful if you want to use Klarna's app features, such as purchase tracking, payment reminders, price comparison, buyer protection, or cashback, without using a deferred payment plan.

Klarna also offers a Pay in full option that lets you pay the full purchase amount immediately at checkout. This is useful if you want to use Klarna's app features, such as purchase tracking, payment reminders, price comparison, buyer protection, or cashback, without using a deferred payment plan.

Is Klarna legit?

Yes. Klarna is a legitimate financial services company that is subject to financial, consumer protection, and privacy laws in the regions where it operates.

For example, in the U.S., Klarna's services may be subject to state licensing requirements, state consumer-credit laws, and federal consumer financial laws, depending on the product. The Consumer Financial Protection Bureau (CFPB) also monitors the broader consumer finance and BNPL sectors.

In Sweden, Klarna Bank AB is authorized as a bank and supervised by the Swedish Financial Supervisory Authority. In the U.K., Klarna Financial Services U.K. Limited is authorized and regulated by the Financial Conduct Authority (FCA) as an Electronic Money Institution, while some BNPL products, such as Pay in 3 and Pay in 30 days, remain unregulated credit agreements. In Germany and other European Economic Area markets, Klarna can provide services through its Swedish banking license and local branches.

Regarding card payments, Klarna is Payment Card Industry Data Security Standard (PCI DSS)-validated, meaning it meets the security requirements for handling cardholder data that it stores, processes, or transmits. Klarna is also subject to applicable data privacy laws, such as the California Consumer Privacy Act (CCPA) and the General Data Protection Regulation (GDPR) in the European Union, depending on the user's location.

Klarna security features

Klarna uses security measures to protect your data and transactions when you shop or make payments on its platform.

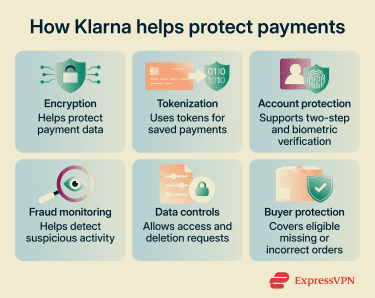

Data encryption protocols

Klarna uses security measures to help protect money and data, including fraud prevention and transaction monitoring. Klarna’s integration documentation also requires that API requests use HTTPS with Transport Layer Security (TLS) 1.2 or later.

Tokenization

Klarna supports tokenization for saved payment methods and future payments. Instead of relying on the original payment details for every future charge, Klarna creates a secure customer token that represents the saved payment method and the customer’s authorization to be charged. For subscriptions, recurring charges, or on-demand payments, the token can be used to authorize future transactions without asking the customer to re-enter payment details each time.

This reduces the need to store, share, or transmit sensitive payment credentials across future transactions.

Authentication

Klarna offers account security options such as two-factor authentication (2FA), biometric login, and passkeys. 2FA adds an extra verification step to help protect your account from unauthorized access. In the Klarna app, you may also be able to use biometric sign-in, such as Face ID, Touch ID, or fingerprint scanning, depending on your device.

Fraud monitoring

Klarna uses machine-learning-powered, real-time fraud monitoring to detect suspicious activity and prevent unauthorized transactions. This can help reduce the risk of fraudulent purchases or account misuse.

User control over personal data

Klarna users have rights over their personal data, including the ability to access information Klarna holds about them and to request its deletion through Klarna’s privacy rights tools, including in the Klarna app.

These rights may vary depending on the user’s location and applicable data protection laws. Klarna may also retain limited information when required for legal, regulatory, or financial obligations, so not all data can always be deleted immediately.

Consumer protection

Klarna's Buyer Protection Policy may apply if an order doesn’t arrive or if the item significantly differs from the seller’s description, such as being incorrect, damaged, incomplete, defective, or counterfeit. If your claim is eligible, you may receive a refund or have your payment obligation removed.

To qualify for Klarna's Buyer Protection Policy, you must:

- Have a Klarna account that’s in good standing (for example, payments are up to date).

- Contact the retailer first and try to resolve the issue directly.

- Provide any requested information or evidence to support your claim.

- Submit your claim within 120 days of purchase.

When you report an eligible problem, Klarna may pause your payment while it reviews the dispute. Klarna then considers the information provided by both the customer and the merchant before deciding the outcome of the case.

Potential downsides

While Klarna can offer convenience and flexible payment options, some plans can carry financial risks, including possible credit reporting, late fees, or interest on longer-term financing.

Impact on credit

Klarna may perform a soft credit check when using certain payment options, such as:

- Pay in 4.

- Pay in 30 days.

- Pay over time.

- The Klarna Credit Card.

Soft checks do not affect a user's credit score and are not visible to other lenders. These checks help Klarna assess eligibility for its payment options. A history of delayed or missed payments may also affect the user's ability to use Klarna’s services in the future.

Credit-reporting practices vary by product and country. In the U.S., Pay over time payment history may be shared with credit bureaus, but for now, the shared data is visible only to the user and doesn't affect the credit score. In the U.K. and other markets, credit checks and reporting practices can vary by product, so users should check the current terms for the specific Klarna payment option they choose.

High-interest rates on long-term financing

Using U.S. terms as an example, Klarna’s Pay over time plans have an annual percentage rate (APR) ranging from 0% to 35.99%, depending on factors such as creditworthiness, loan term, and credit approval.

At the higher end, these rates can exceed average U.S. credit card rates and many traditional personal loan rates.

How to use Klarna safely?

Klarna uses strong security measures similar to those used by other major payment processing platforms. However, safe use also depends on how you manage payments, protect your account, and shop online. Below are practical tips for reducing financial risk and staying protected.

Set payment reminders

Klarna sends payment reminders by email, text, or push notifications shortly before payments are due, depending on your location and notification settings. It can still be useful to set your own reminders or calendar alerts so you can see upcoming payments in advance and, where applicable, reduce the risk of missed payments or fees.

Only spend within a set budget

BNPL services can make spending harder to track, especially when you have multiple payment plans at once. A safer approach is to treat each Klarna purchase as if the full amount is already deducted from your available balance.

Secure your account

Since Klarna accounts are tied to financial activity, it’s important to protect them like you would a banking app. Use a strong, unique password and enable 2FA, biometrics, and/or passkeys.

If you have trouble remembering long, complex passwords, a password manager can help. ExpressVPN's password manager, ExpressKeys, stores passwords in a secure digital vault, helps create strong passwords, autofills login details, and can generate 2FA codes for supported accounts.

Watch out for phishing scams

Phishing scams involve fake emails, texts, or websites that appear to be from Klarna. These messages may claim that there’s a payment issue or account problem and urge users to click a link or log in to resolve it.

Clicking a link or entering login details on a fake page could expose accounts or personal information, potentially contributing to identity theft or BNPL fraud. As a fraud prevention measure, avoid responding to unexpected messages; instead, open the Klarna app or website directly to check your account status.

Use secure devices and networks

Avoid accessing Klarna on shared or public devices or on public Wi-Fi, as these environments may be less secure. If you need to use Klarna on a public network, a virtual private network (VPN) can add a layer of protection by encrypting your internet connection.

Keep proof of purchases and returns

If you ever need to dispute a charge, Klarna may ask you to provide valid evidence to support your case. This can include proof that you contacted the retailer, shipping or tracking information, return tracking details, or other documentation related to the issue. Clear documentation can make the dispute process easier and help Klarna assess your claim.

Who should use Klarna?

Klarna may be better suited for people who can comfortably manage upcoming payments and use it for payment convenience rather than to stretch their budget. A good use case, for instance, is splitting a purchase you could afford upfront to keep cash flow flexible.

Klarna may be less suitable if installment payments make it harder to stay within budget, encourage purchases that would otherwise be out of reach, or make it difficult to track upcoming payments.

FAQ: Common questions about Klarna’s safety

Does Klarna affect your credit score?

The Pay over time option may be reported to credit bureaus, but the impact varies by region. In the U.S., Pay over time payment history may be shared with credit bureaus, but the shared data is currently visible only to you and does not affect your credit score. In the U.K. and other markets, credit checks and reporting practices can vary by product, so check the terms for the specific Klarna option you choose.

What happens if you miss a Klarna payment?

Can you get a refund through Klarna?

To be eligible, you'll need to have a Klarna account that’s in good standing, contact the retailer first to try to resolve the issue directly, provide information or evidence to support your claim, and submit your claim within 120 days of purchase. Klarna then reviews the case before making a decision.

Does Klarna charge fees or interest?

Can using Klarna hurt your budget?

Is Klarna a good idea for large purchases?

Explore the web with greater privacy

Get ExpressVPNSign up today for a chance to win FIFA World Cup 2026™ tickets.